Broker roundup: Profit warning edition

Cyclical or structural? Structural!

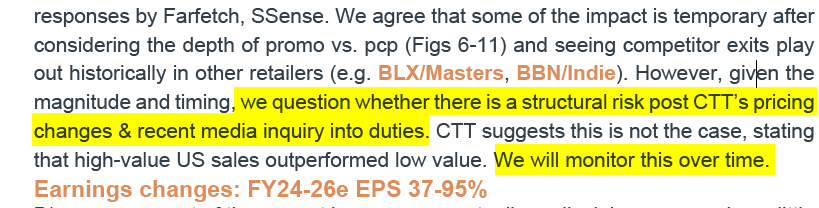

After Cettire’s stonking profit warning and 50% fall on Monday, Tuesday’s dead cat bounce transmogrified (trans-moggy-fied?) into a rather pathetic feline pavement pizza. Perhaps this can be explained by the revelations in the AFR and in these pixels that Cettire had been playing the old switcheroo with HS codes which lowered duties paid, but more likely it was because the profit warning itself was so swingeing and aligned with the predictions made about the expected effects that the changes to Cettire’s pricing model would have that even the traditionally bullish Aussie sell side community - with one entirely expected exception - had to admit that this moggy was a bit whiffy.

Gold Five: Stay on target

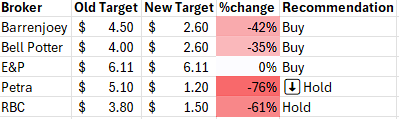

A table of the price target changes tells its own story:

Inevitably we have to address friend of the show, POI and eternal optimist Julian Mulcahy’s basis for maintaining his hilariously priapic and monodirectional target price in the face of what even he describes as a weaker than expected trading update. Despite cutting his NPAT numbers for FY24/25 by -35%/-19%, Julian stays on target!! How? Because the valuation is based on FY26 numbers which remain remarkably unmolested. Presumably in Julian’s world, the Titanic was a FY1914 story.

The sensible centre

Moving on to what we might characterise as the more sensible members of the analyst community, we begin to see how Damascene, scales have started to become detached from various retinas.

Long term sell trading hold RBC are characteristically cagey in their analysis, with Wei-Weng pointing out variously that China is unlikely to be a growth panacea, that a buyback would be tantamount to seppuku and that Cettire have confirmed that they will be taking unquantified “one-off” charges below the line - something that no broker appears to have factored into their numbers. Wei-Weng also raises the question as to whether this disastrous guidance can be attributed solely to the softening luxury market or whether scrutiny of Cettire’s business practices has been a contribution factor - who could have guessed? Oh that’s right!

Somewhat surprisingly Sam Haddad at Petra came out with the most visceral downgrade, cutting his target 76% whilst downgrading CTT to hold. Sam also raised the point that by participating even ‘selectively’ in promotions, Cettire’s eroded pricing advantage means that they might have to fund these discounts themselves - something the EOFY 10% sale currently running on the Cettire website brings into focus.

Chami at Bell Potter has a habit of repeating company lines verbatim however even she cut her target to 2.60, a mere 130% above last price. This is practically a sell note! Much like the company, Chami attributes the downgrade exclusively to cyclical factors and awaits eagerly the return to ‘normal’. What if this is normal Chami?

We can help Ari

Now of course we’ve saved the best for last - Ari at house broker Barrenjoey. Whether he is still pink satin shirt-festooned is unclear, however from what we have previously characterised as his hostage cell tapping out messages to his potential rescuers, so far managing to deliver us the FSFE loophole and de minimis impacts - we receive the most bearish buy note in market memory.

Of course Ari cuts his price target - after all, how could anyone sensible not do so in the face of such evidence?1 - however it’s in the details that the full extent of Ari’s underlying ursine nature becomes apparent.

Whilst almost apologetically attempting to gain cover from his captors by basing his target on FY26 earnings like Julian, Ari cuts his earnings estimates to the bottom of the market, wiping out any profit in FY25 and hacking back FY26 earnings by 40% - Ari finds the courage to say this is based on a scare-quoted ‘snap-back’ to something approaching the status quo ante scrutiny, something it’s clear he doesn’t really believe. Indeed, so low is his conviction he points out that CTT could be a zero if it’s not just cyclical.

Trust in the gnomic emissions of Cettire this is not, and after how Ari was treated in the client duties call in March, there can be little wonder why. When you sow the wind…

Small world

One intriguing detail in Ari’s note is in one of the least expected places - the name of the associate, one Taylor Guyot. Now Guyot is a rare name, but a storied one in funds management since the co-portfolio manager of Regal’s hitherto stellar performing Smaller Companies fund and 15% Cettire investor is none other than Todd Guyot. Discreet inquiries have confirmed this is no coincidence and that Taylor is indeed Todd’s daughter.

Whilst it’s fun to play with the conceit that Ari is a hostage to the imperatives of his employer’s interests and it’s tempting to imagine for comic effect that Ari’s Excel finger is held in a vice by a Regal plant, this would be unfair and demeaning. Everyone has the right to make their way in the world and since I have never met Taylor, I can only assume that she is scrupulously fair in her analysis of Cettire and a fully formed independent human being entirely apart from her vocally long Cettire father. But much like Cettire’s founder’s sister defending the ASX against the iSignThis’s comical fabulation of a lawsuit it goes to show that it can be a small world, and in Australia it’s smaller still.

You do it to yourself, and that’s why it really hurts Julian!