Cettire Key Audit Matters

Giving Grant Thornton a helping hand

For each of the three Annual reports that Cettire has filed in its time as a listed company its auditor Grant Thornton has listed the same three Key Audit Matters (KAMs) in the annual report, which can be characterised as:

Revenue recognition: AASB 15 - whether performance obligations have been met at period end to book revenue

Intangible assets: AASB 138 - whether costs can be capitalised and if any of the intangible assets generated require impairment

R&D tax incentive: AASB 120 - whether the claimed spend is eligible for the tax incentive that has been claimed.

Repeatedly marking the same scorecard is all well and good, however since scrutiny on the company has increased precipitating multiple changes in prior business practices, it seems only right that any auditor attempting to abide by audit standards in keeping the user of financial statements front of mind whilst conducting an audit should keep an open mind about what constitutes a Key Audit Matter.

Indeed after Grant Thornton and partner Brad Thompson were both charged by ASIC over the 2018 audit of iSignThis (hey Yianni!), it is sincerely hoped that this the issues raised in this open letter to Grant Thornton, ASIC, ASX compliance and the AUASB (the auditing standards board) allows the audit of Cettire to give confidence to the market in the integrity of the accounts, or failing that to ensure that the beefed up penalties for failing to conduct an audit with due care and diligence under strict liability finally result in some time in the clink for gatekeepers to the financial system that fail in their duties. I’m pretty agnostic as to the outcome!

To whom it may concern

Re: Cettire’s FY2024 audit

Please find following a list of what are clearly relevant to the conduct of the audit and Key Audit Matters for Cettire.

HS code switching might imply a dual system

As documented by the AFR and taxloss.substack.com, Cettire charged a customer duties based on one HS code but declared a different HS code to CBP. Not only is this prima facie customs fraud, but in order to rule out that this is pervasive and that Cettire’s systems contained one HS code for customers and a different HS code to declare to Customs, an auditor should investigate the customs flow of a large sample of high cost items (over USD1250 would be a good start) which attract a duty of 15% or higher which were shipped DDP and had cash duties paid on them by Cettire which were sold into the US prior to March 2024 . This investigation should track the transaction from sales basket to invoicing through to customs entry and ensure that each item matches in valuation and HS code.

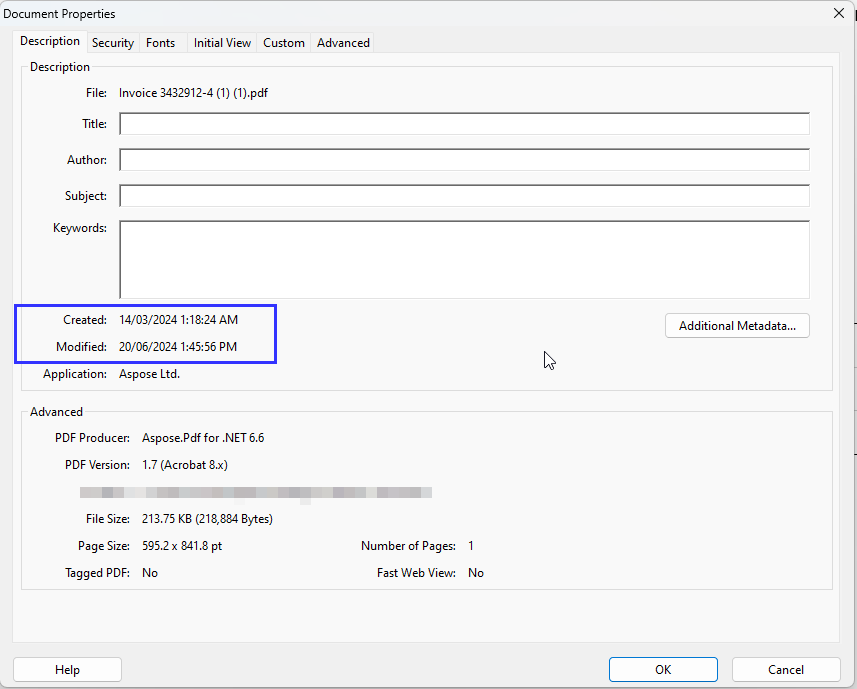

Suspected editing of invoices requires an auditor to show professional scepticism

As part of our investigations into Cettire, we requested an invoice for a test purchase into the US which was made in March. After an extended run around, after the threat of a chargeback and a report to the ATO, we received an invoice in June. The metadata of the pdf See footnote1 had a discrepancy between the creation date of the file and the modified date, which might imply that the invoice is not reflective of the underlying system that generated it, on which it is assumed any audit will be based.

ASA 200 requires that an auditor uses Professional scepticism, including being alert to conditions which may indicate possible misstatement due to error or fraud. If internal accounting systems did not agree with an edited invoice, this would clearly qualify as such a condition.

An auditor should investigate any discrepancies in invoices provided to customers and the underlying entries in Cettire’s accounting systems. This should also include a search of Cettire’s customer service emails to identify where an invoice has been requested and not provided.

Ark International Pty Ltd and US sales taxes

Ark International is the Cettire entity that has been identified as registered for sales taxes in various US states. After the Wayfair ruling, US state law is relatively uniform in requiring any entity that has sales over a threshold to register and pay sales taxes in that state, and this is based on these sales establishing an “economic nexus” in the state. The major states (and presumably many others) do not allow a related party to register for sales taxes, it has to be the entity that has made the sale to the customer in that state, which implies that to be compliant with US sales tax law Ark International would need to be the entity that sold goods to the end customer.

However in our case the invoice that Cettire provided to DHL identifies Ark Technologies as the exporter, begging the question which Cettire entity has nexus in the various US states.

If there is a complex series of transactions from supplier to various Cettire entities to the ultimate customer that somehow allow Ark Technologies to be the exporter but Ark International to be the entity that has established nexus and is paying sales taxes in the US - have these all been recorded correctly?

Deed of Cross Guarantee for Ark International

Ark International filed a deed of cross guarantee with ASIC on 28 June 2024. This exempts it from filing audited accounts with ASIC for FY24. However it does not exempt them from this requirement for FY23 or prior years. If Ark International did not meet the criteria for a “small proprietary company” during FY23, then it should have audited accounts filed. However since its only filings since its registration in 2021 are the April/May 2024 appointments of Tim Hume and a non-exec as directors it’s also open to investigate if any transactions have ever flowed through Ark International. If it has been effectively dormant, then Cettire has not been registered correctly for sales taxes in the US for its entire existence.

Duties Revenues, Duties Costs - not material but significant

The company stated that duties revenues were not material to revenues, that duties costs were not material to costs, and that net duties revenues were not material to profits. Given the scrutiny on Cettire’s duties practices, the figure charged to customers, the amount paid to customs and the net amount of duties revenue should be disclosed, having been rigorously checked for any alteration.

First Sale For Export and De Minimis

The First Sale For Export (FSFE) rule allows companies to declare a lower value to customs in order to reduce duties payable. However my prior understanding of this was faulty, but not in a good way for Cettire! FSFE can be used to reduce duties payable, but the Customs code is very clear that De Minimis valuation is based only on the retail value. So for example, a $1000 retail item that is declared with a $700 FSFE valuation at the border is still liable to duties on the $700, since the retail value was over $800. Awks!

The auditor should investigate sales to customers in the range of USD800-1140 to see if the correct duties have been paid in order to be assured that a liability to CBP doesn’t exist around these items, which would represent a material misstatement.

What is the nature of Accounts Receivable in a business that takes payment upfront?

The nature of Cettire’s receivables has not been disclosed before, however it has been suggested that they relate in large part to card scheme rolling reserves or by Regal as “simply money due for input VAT or GST credits”. If a 15% holder that is close to the company is confused then this requires further disclosure to ensure the balance sheet accurately reflects what users of the financial statements expect.

Asking questions of the right people

The auditor is required to appear at the company AGM. Each of these matters will be raised so it’s important that the auditor is on notice of this.

These Key Audit Matters are in addition to the KAMs that Adam Pitts identified in FY21 and FY22, and that in what one can only presume was some sort of mind meld, Crystel Gangemi also identically identified in FY23. One thing I’m interested in is how Cettire have received R&D incentive payments when they say they have outsourced their tech to China - do Cettire hold an Advance and Overseas Finding (AOF) for these activities?2 R&D activities must be undertaken in Australia unless an AOF is held by the company.

https://www.pwc.com.au/pwc-private/r-and-d-gov-incentives/tax-incentives/Claiming-the-RD-offset-for-expenditure-incurred-on-RD-activities-conducted-outside-Australia.html#:~:text=The%20R%26D%20Tax%20Incentive%20program,(AOF)%20for%20those%20activities.

I think people's perception of the scope and detail of audits is far greater than it actually is. You have to remember, auditors only audit the financials. They really do not look too deeply into the legality of the business and business practices. It is essentially an audit of the accounting function of the business. Ultimately, the directors sign on the financials - they are the ones who oversee the business and they are the ones who should bear most of the responsibility.

As an auditor myself, I doubt that the below points you touched on will be dealt with by the auditors:

- HS code switching - depends how material the duties expense is, but if it is material, they might do substantive testing on the duties balance. This could involve getting a breakdown of revenue by HS code and coming up with an expected duties expense based on that revenue breakdown. In saying this, it is not the role of an auditor to intervene on the operations of the business and force them to make payments if something is wrong. Auditors are not experts on international duties laws, nor do they have time to look into these matters deeply - this is ultimately a matter for the client. Same principle applies for FSFE.

-Ark International - again, auditors are not legal experts and can not determine if Ark International has established an 'economic nexus' in the respective state.

-Duties revenue and costs - it is my understanding that as long as the financial statements comply with accounting standards in respect to disclosures, the client can map their financials however they like and hide duties revenue and duties costs in P&L line items.

However, the below points will likely be touched on:

-Editing of invoices - if invoices have been edited, a corresponding GL entry has to be made to reflect that change (assuming the $ amount is being changed). Auditors will be making sure that invoices agree to GL for both revenue and expenses testing.

-Accounts receivable - as the balance was quite material at the HY, auditors will have to test the account. If it is due to GST receivable, testing would probably involve agreement to BAS statement.

Another thing to mention is that the staff from probably manager down are often oblivious to what is going on with the client in the real world (in other words, they are just there to do a job, and they don't read the AFR and understand what to look out for). This is just one out of about ten clients that they will deal with over the busy period and they will very likely just roll-forward what was done last year without applying a whole lot of skepticism. Hopefully though, the partner has put the fear of God into them to not stuff CTT's audit up.

Note: Above views are my own.